Audit Assertions for Purchases

Accounts payable is usually one of the more important audit areas. Whilst the procedures are perhaps similar in nature their purpose and relevance is to test different assertions regarding inventory balances.

Understanding Audit Assertions A Small Business Guide

By inspecting the invoice.

. A opening and closing inventory balances. These are compliance requirements that are subject to the compliance audit. When the office supplies are utilized during the month an audit adjustment entry will be made to credit prepaid office.

Most of the business prefer to make the payments by banks transactions to minimize the fraud case. An auditor most likely would limit substantive tests of sales transactions when control risk is assessed as low for the existence or occurrence assertions concerning sales transactions and the auditor has already gathered evidence supporting. 8 Audit Risk describes audit risk and its components in a financial statement audit the risk of material misstatement consisting of.

This could be the result of intentional fraud or. Modification as used in this subpart means a minor change in the details of a provision or clause that is specifically authorized by the FAR and does not alter the substance of the provision or clause see 52104. For an auditor to be reasonably assured of the Cash Disbursements made by the entity tests will be performed to cover the audit assertions.

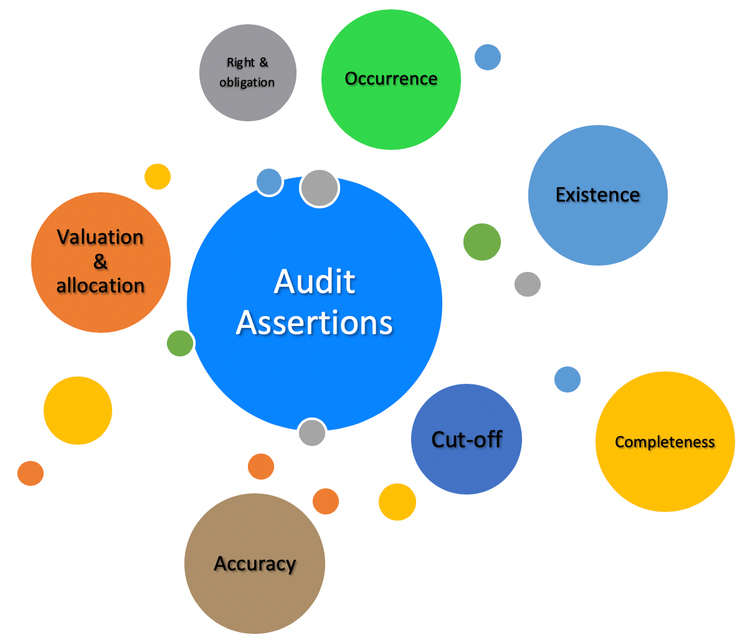

Substantive procedures are the method or audit tests designed by an auditor to evaluate the financial statements of the company which require an auditor to create conclusive evidence for verifying the completeness accuracy existence occurrence measurement and valuation audit assertions of the financial records of the business. Sales purchases and account balances eg. In this post Ill answer questions such as how should we test accounts payable.

Cash purchases have happened when an entity makes a purchase of goods or renders the services and then makes the payments by cash immediately. Observing the distribution of paychecks. The audit risk for Cash Disbursements is generally low but it also heavily depends on how well the entitys internal control policy is.

If we disregard stock purchases and sales equity is usually the accumulation of retained earnings. Confirms sales values and purchases costs ie. See page 64 and Chapter 16 of the notes assertions relate to classes of transactions eg.

B Numbering 1 FAR provisions and clauses. Collectively all classes of transactions account balances and their related disclosures make up the financial statements. Prepaid expenses are known as assets that are being paid for and then used gradually during the accounting period ie office suppliesA company purchases and pays for office supplies and as they are consumed they will become an expense.

The assertions applicable to Cash Disbursements are. Inspecting payroll tax returns. In order to audit the accounts payable it requires to use the combination of analytical procedures and tests of detail or substantive audit procedures for accounts payable.

B cash receipts and accounts receivable. When control risk is assessed as low for assertions related to payroll substantive tests of payroll balances most likely would be limited to applying substantive analytical procedures and A. The following are the accounting records for both purchases on credit and cash purchases.

Put the relevant assertions next to each audit stepthis makes the connections between the RMMs at the assertion level and the audit steps clear. First its easy to increase net income by not recording period-end payables. Subpart 522 sets forth the text of all FAR provisions and clauses each in its own separate subsection.

For a detailed list of accounting audit definitions see PCAOB document AU 801. Thus in this section we will take some assertions that we usually test in. And should I perform fraud-related expense procedures.

This includes details collected during an audit that allow an. One high risk of inventory is that the company bought the inventory but the purchases were not recorded into the inventory account. Footing and crossfooting the payroll register.

As auditors we usually audit inventory by testing the various audit assertions including existence completeness rights and obligations and valuation. These aspects of audit risk are sampling risk and nonsampling risk respectively. Typically we perform the audit of accounts payable in conjunction with the audit of purchases.

Second many forms of theft occur in the accounts payable area. And retained earnings comes from the earnings or losses on the income statement. Information that the auditor must report as part of a prescribed audit.

Audit Expenses Assertions Risks And Procedures Wikiaccounting

Audit Procedures Types Assertions Accountinguide

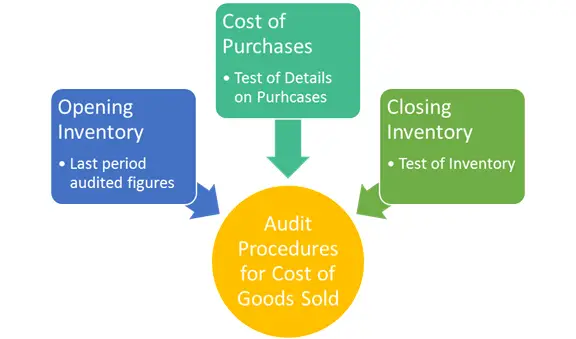

Auditing Cost Of Goods Sold Risks Assertions And Procedures Audithow

Inventory Audit Assertions Substantive Tests Youtube

No comments for "Audit Assertions for Purchases"

Post a Comment